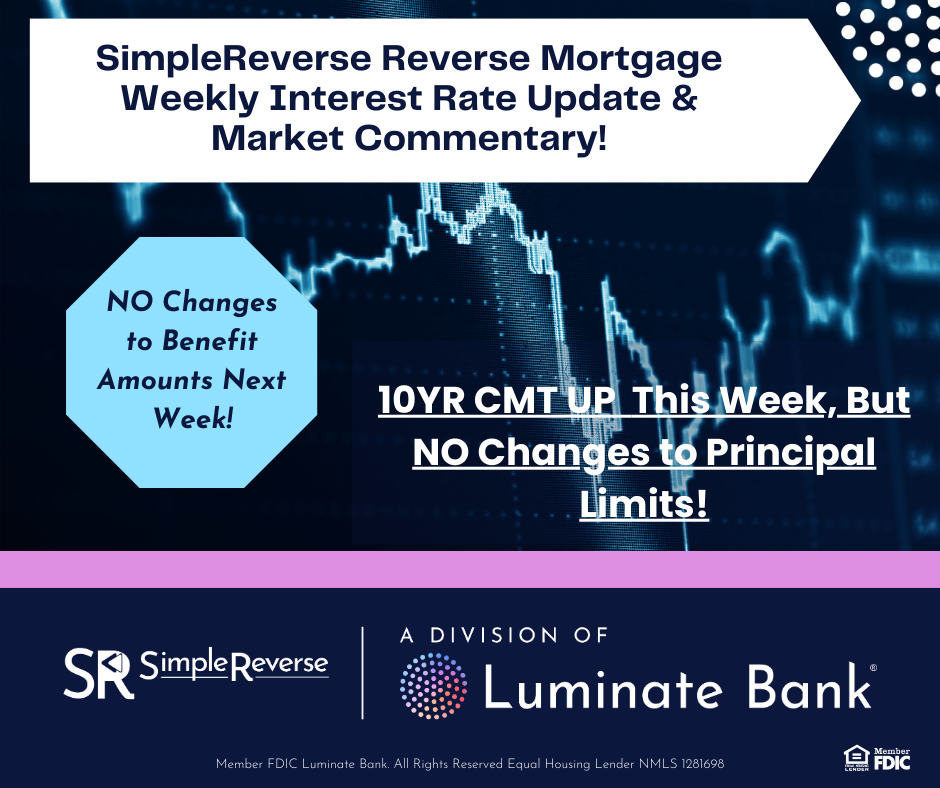

The 10YR CMT continued its move back up this week, and we will see an INCREASE in the 10YR CMT for next week. But, this will result in NO CHANGE to PRINCIPAL LIMITS and BENEFIT AMOUNTS next week!!

The 10YR CMT currently sits at 4.08% for this week, and we will see

an increase of 7-9 bps

in the Expected Rate next week! However, this will have

NO IMPACT on the Expected Rate and will result in the SAME Benefit Amounts next week!

Data was released today on the FED’s preferred inflation measure, Personal Consumption Expenditures (PCE), and the Core PCE number held steady at 2.9%, while Headline PCE data came in slightly higher than last month at 2.7%, but in line with forecasts. PCE remains above the FED’s target of 2%, analysts still expect at least one more rate cut from the FED this year in response to the softening labor market. Unemployment is still relatively low at 4.3%, but the labor market does appear to be cooling but not collapsing. Analysts do expect to see inflation rise further in the short-term, as higher import costs are partially passed along to consumers, but they believe these should be near-term hikes that aren’t ongoing drivers of inflation.

The new upcoming risks to the markets include the ongoing political divisions in Washington and the continued real probability of a government shutdown at the end of the current fiscal year, quickly approaching next week on September 30. A shutdown of the federal government would begin on October 1 if Congress fails to pass a stopgap measure (continuing resolution) or the necessary appropriations bills. Shutdowns have become more commonplace in recent history but usually don’t last long. The longest was in December of 2018 which lasted for 35 days. Analysts do expect a short-term slowdown in growth around a shutdown, but also a quick recovery in the months after. The longer the possible shutdown the more impact on the markets as financial markets certainly don’t like uncertainty. However, the markets to tend to be driven more by the outlook for economic growth and earnings, as opposed to the political landscape.

Finally, we have heard from several members of the FED this week on their views on the economy after last week’s rate cut; and those comments do indicate some disagreements and differing views on how to move forward. Chair Powell reiterated his messaging that rates should be moving to less restrictive levels, but he didn’t provide a great deal of clarity over timing and the extent of those adjustments. Others have been more dovish, warning that more decisive actions on cuts needs to be made sooner rather than later. More data will be coming before the FED heads into their next meeting in October.

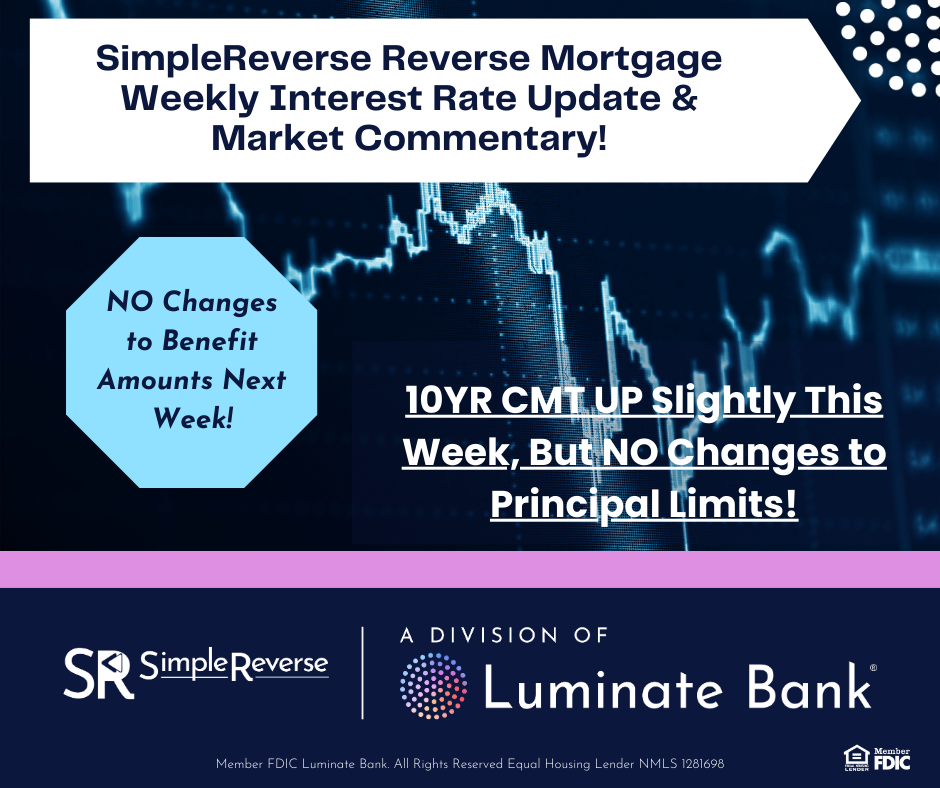

This week, the 10YR CMT Index is 4.08%. Here is what the 10YR CMT has done this week, so we will see an INCREASE in the 10YR CMT for next week. This increase WILL HAVE NO IMPACT on Benefit Amounts!

10YR CMT

9/22/25 9/23/25 9/24/25 9/25/25 9/26/25 (Intraday)

4.15 4.12 4.16 4.18 4.18

Based on the data from this week, we will see an INCREASE in the Expected Rate of 7-9 bps for next week. This INCREASE will have NO IMPACT on the Principal Limits and Benefit Amounts for next week. So, if you have applications or closings soon, there will be

NO DIFFERENCE IN BENEFIT AMOUNTS FOR YOUR CUSTOMERS IF YOU TAKE APPLICATIONS NOW OR WAIT UNTIL NEXT WEEK! As usual, new rates for next week will take effect on Tuesday, 9/30/25 and beyond! As always, we are simply providing this data to you, so that YOU can continue to make the decisions that best suit your business based on the information you have!

If you have questions about this, please let me know right away!!! Thanks for the partnership and Good Selling!!!